By Agroempresario.com

The US retail market for plant-based meat is facing a significant downturn. According to new data from SPINS shared with AgFunderNews, retail sales of plant-based meat in the United States fell 7.5% to $1.13 billion in the 52 weeks ending April 20, 2025. Unit sales were down 10%, revealing deeper structural challenges for this once rapidly expanding category.

Plant-Based Meat Sales in Decline

In a sharp contrast to the early excitement surrounding brands like Beyond Meat, the plant-based meat industry now faces reduced consumer demand, pricing pressures, and narrowing shelf space in supermarkets. Refrigerated plant-based meat—once the engine of growth—fell 12.1% in dollar sales, reaching $349.7 million. Units were down 14.4%.

Frozen alternatives, which represent nearly 70% of the plant-based meat market, showed slightly better resilience with sales dropping 5.3% to $782.3 million. Unit sales in this segment decreased 7.8%.

Some subcategories still managed to record growth, albeit modest and from a small base. These include refrigerated cutlets, strips, and nuggets (+8.3%), refrigerated dogs (+1.9%), seitan (+1.7%), and frozen loaves and roasts (+0.7%). However, these gains were not enough to offset overall declines.

Particularly hard-hit were refrigerated plant-based burgers, once a retail centerpiece, which suffered a dramatic 26% year-over-year drop.

Retailers Reduce Plant-Based Assortments

The declining numbers are accompanied by a trend of reduced shelf space for plant-based meats. According to data from 210 Analytics, the average number of refrigerated plant-based items per store dropped to 9.7 in April 2025—a 10.3% year-over-year decline and a staggering 31% fall since early 2021.

Brands like Beyond Meat have acknowledged this contraction, noting that some products are being shifted to frozen aisles or removed entirely.

In contrast, conventional meat continues to thrive. Circana data shows US retail sales of fresh meat rose 6% over the same period, with volumes up 2.7%. Frozen processed meat and poultry rose by 10.9% in sales, while frozen unprocessed variants increased by 4.2%.

Category Breakdown

Top Frozen Categories (52 weeks to April 20, 2025):

-

Nuggets, strips, cutlets: -6.8% to $296 million

-

Burgers: -4.1% to $209 million

-

Breakfast meats: -5% to $129 million

-

Grounds: -4.7% to $47 million

Top Refrigerated Categories:

-

Grounds: -14.1% to $82 million

-

Sausage links: -14.4% to $71 million

-

Deli meats: -4.9% to $44 million

-

Burgers: -26% to $40 million

Household Penetration and Pricing Challenges

According to the Good Food Institute (GFI) and the Plant Based Foods Association, plant-based meat penetration in US households has plateaued at 13%, while plant-based milk holds at around 40%. Price remains a key issue: most plant-based products cost two to four times more than their conventional counterparts.

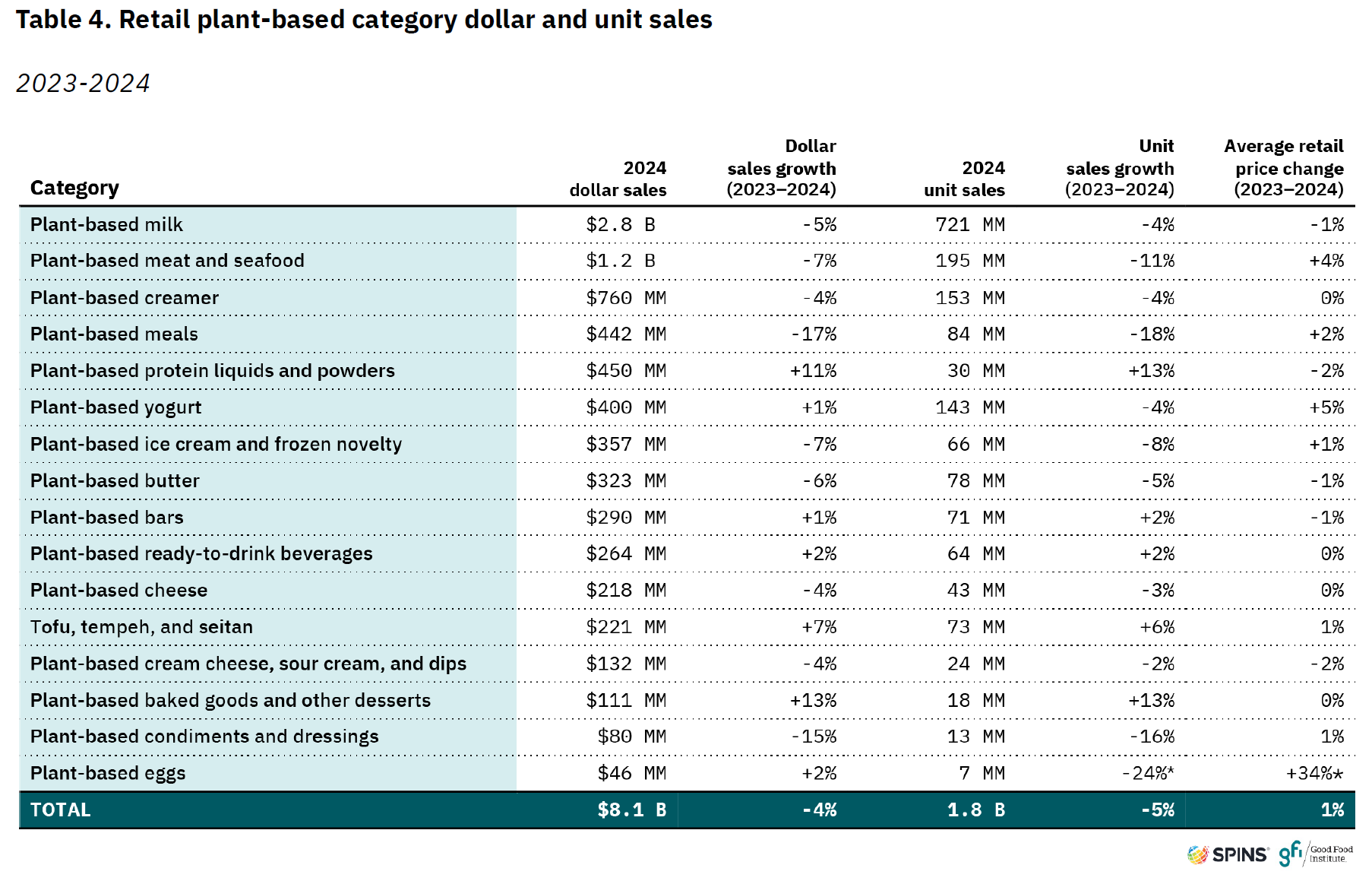

Overall, US retail sales of plant-based foods dropped 4% in 2024, totaling $8.1 billion, with unit sales down 5%. Plant-based meat and seafood specifically fell 7% to $1.2 billion in 2024.

Yet, some categories, such as tofu, tempeh, plant-based protein powders, RTD beverages, and desserts, saw growth. According to the GFI, these "pockets of growth" indicate consumer interest remains alive in certain niches.

Plant-Based Foodservice: A Mixed Picture

In the US foodservice sector, the plant-based meat category experienced a 5% drop in 2024, but there were silver linings. Plant-based pork, chicken tenders, chorizo sausage, tofu, and tempeh recorded gains. Plant-based milk also grew in this segment, with a 9% rise in dollar sales and 6% in volume.

Perhaps most notably, plant-based eggs surged 28% in foodservice sales in 2024—albeit from a very low base. With rising prices of animal-based eggs due to avian flu outbreaks, this niche could expand further in 2025.

A Global Glimmer of Hope

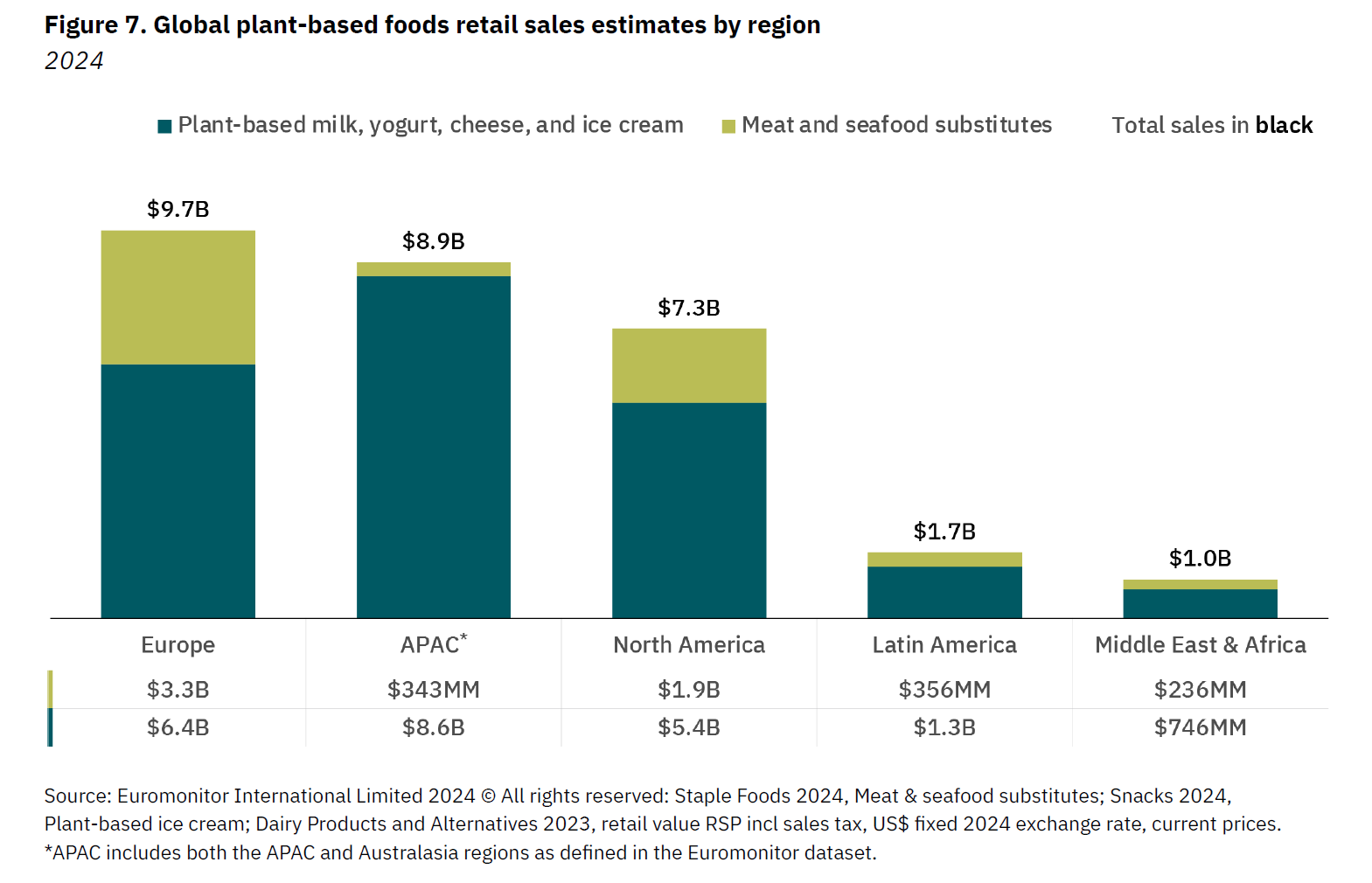

Internationally, the outlook appears more optimistic. According to Euromonitor data cited by the GFI, global retail sales of plant-based meat and seafood rose 4% to $6.1 billion in 2024. Global sales of plant-based dairy products grew 5% to $22.4 billion, with milk making up over 80% of these figures.

Interestingly, the plant-based cheese category grew by 11%, outpacing the traditional dairy sector, signaling strong potential in international markets.

Investment and Industry Consolidation

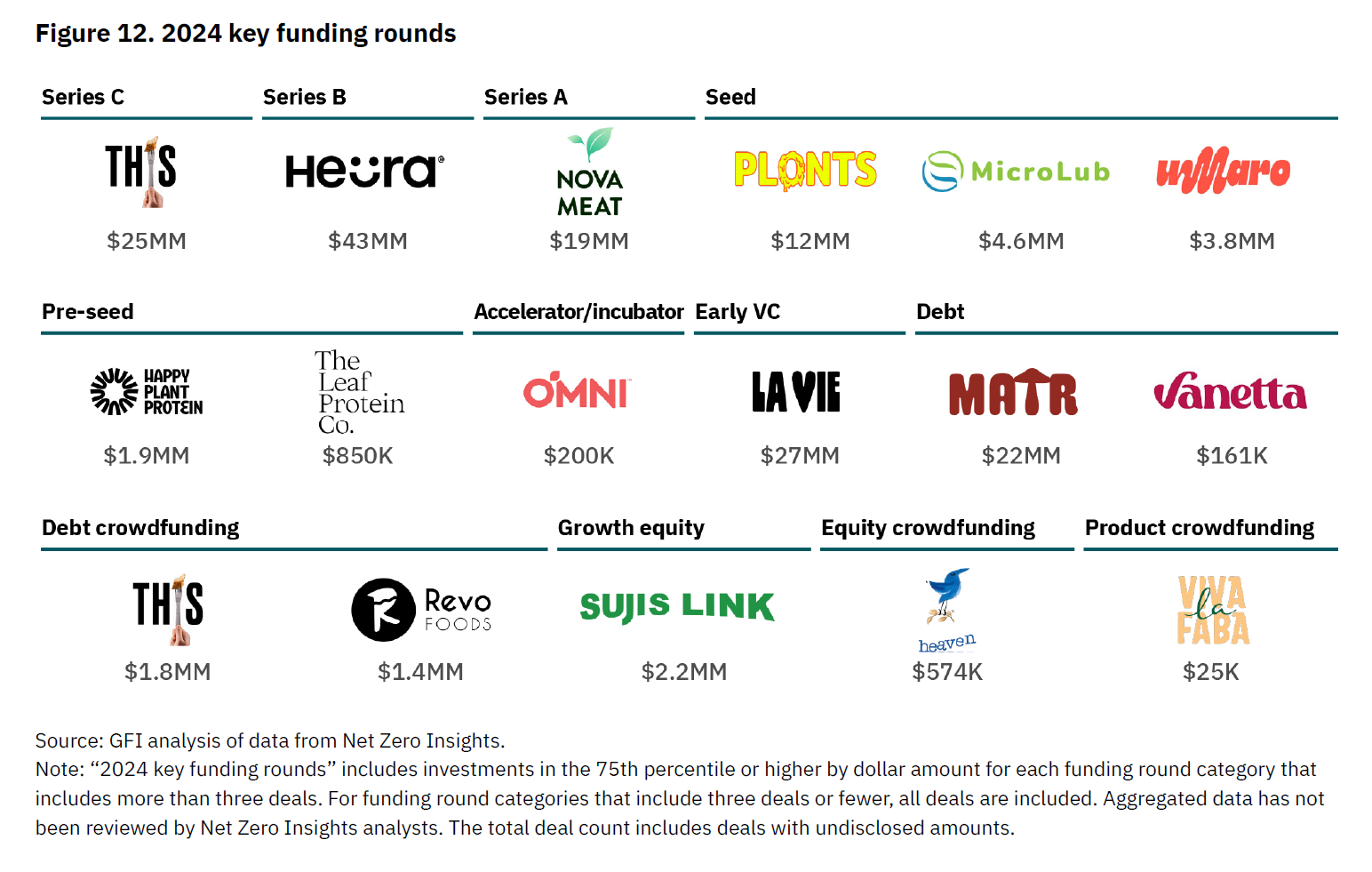

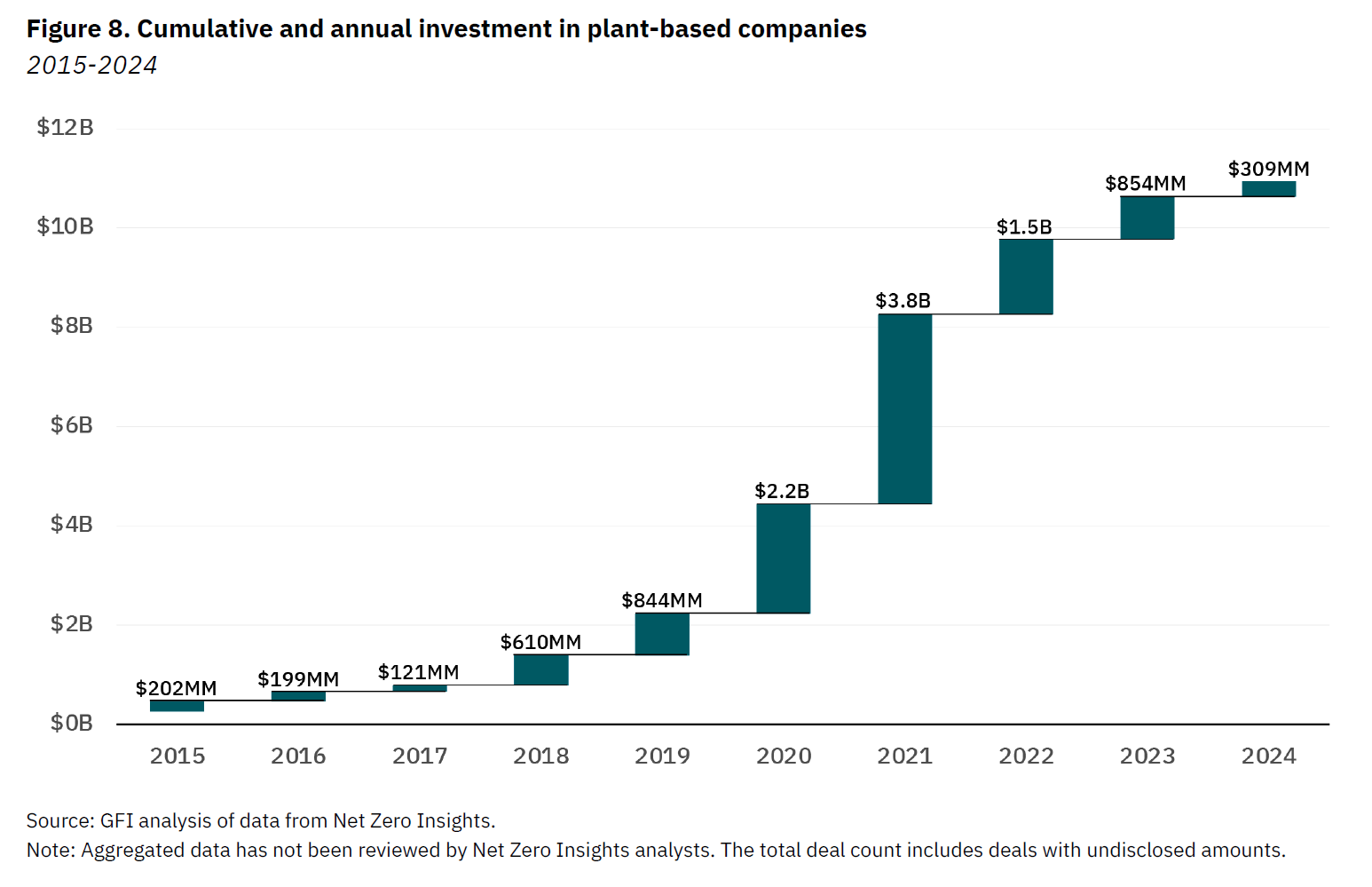

Investor confidence in the plant-based sector is waning. Funding for startups developing plant-based meat, dairy, and eggs plunged 64% in 2024, dropping from $854 million to just $309 million, according to the GFI.

The decline follows a broader cooling in venture capital activity, especially after the peak funding levels during the low-interest era of 2020–2022. The lack of successful exits and continued sales struggles has triggered mergers, downsizing, and even closures across the sector.

However, the GFI notes that consolidation is a natural stage in any industry’s evolution. While some companies disappear, others will merge, license IP, or pivot—steps that can ultimately strengthen the plant-based ecosystem through shared expertise and economies of scale.