By Agroempresario.com

A quiet reordering of innovation in the global food system is underway. While headlines often highlight robotics, vertical farms, or the latest in gene editing, the most consequential shifts are unfolding beneath the surface. They are fundamentally shifting who decides what we consume, who owns critical assets, how capital is deployed, and how biology and climate converge. These systemic undercurrents—subtle yet profound—are defining the next decade of agricultural innovation.

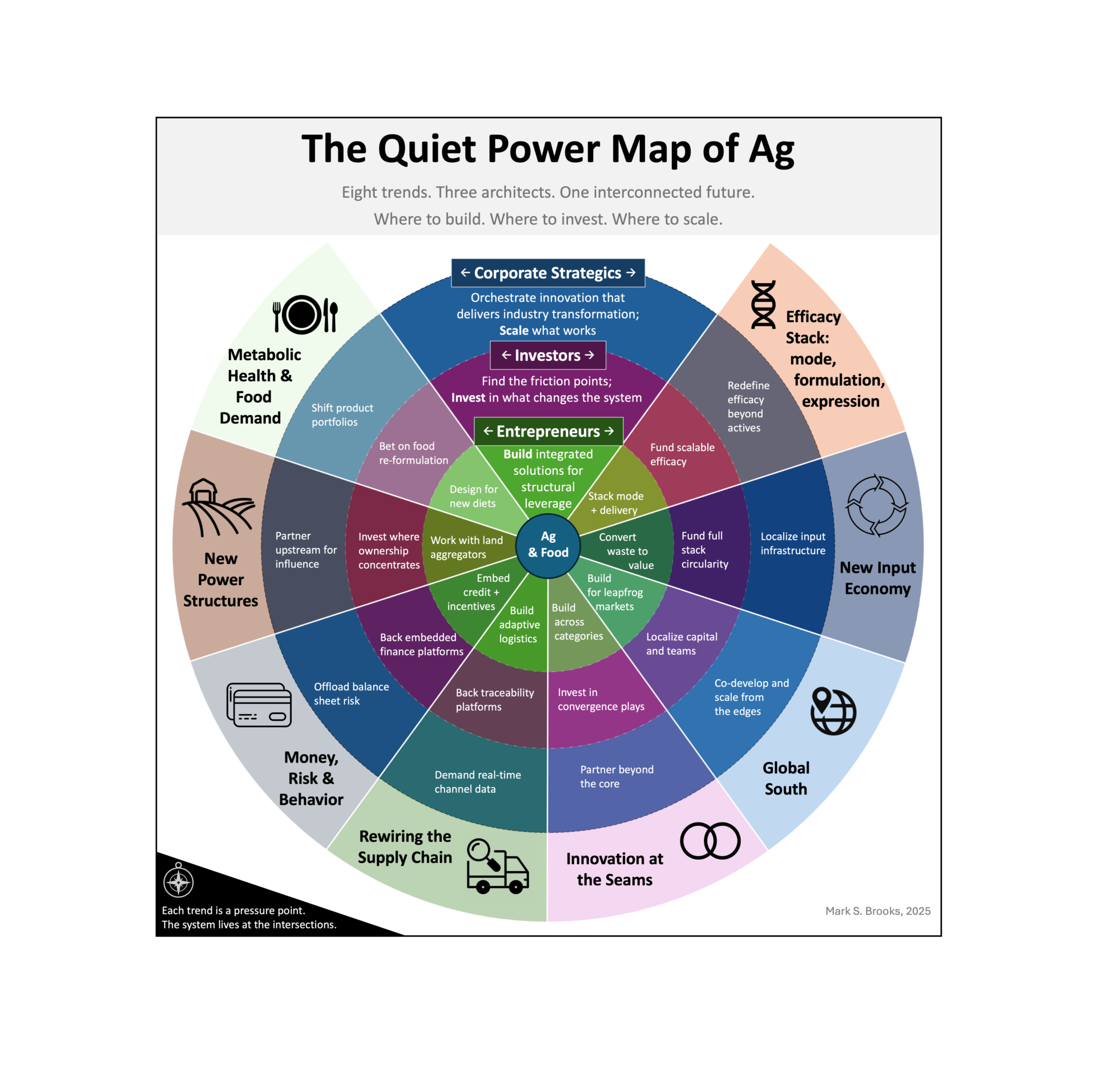

To truly grasp where opportunity lies, we must see beyond yield. This is not a product story; it’s a systems story. Eight emerging trends are quietly converging, inviting builders, investors, and corporates to act at the seams where capital, power, biology, and climate intersect. Below, we outline each trend, explain why it matters, and what it implies for each stakeholder group.

Metabolic Health & Food Demand

The advent of GLP‑1 drugs—such as Ozempic and Wegovy—is reshaping consumption patterns. These medications don’t just impact weight—they revolutionize metabolism and appetite, reducing the demand for calorie‑dense processed foods and increasing consumer preference for functional nutrition, richer in fiber and protein.

- Why it matters: The shift is not marginal. As more consumers use GLP‑1s, entire commodity chains could pivot toward healthier, lower‑calorie ingredients.

- Investor signal: Companies developing high-fiber snacks, plant proteins, and nutrient-enriched ingredients stand to benefit.

- Builder call: Build food products aligned with this emerging demand—think fiber-rich beverages or modular protein blends.

- Corporate action: Food majors should reposition portfolios toward health-conscious products, anticipating demand shifts.

New Power Structures in Agriculture

Agricultural private equity (PE) has moved beyond farming equipment into purchasing farmland, retail networks, and agronomic services. PE now treats land as an asset class, reshaping decision-making lenses toward IRR rather than yield alone.

Simultaneously, distributors are evolving into market-makers by white-labeling startup innovations (biologics, chemistries), providing new go-to-market avenues independent from major agribusiness players.

- Implications for startups:

- Demonstrate how your solution improves land value and cash flow.

- Build relationships not just with farmers, but with PE owners and distribution networks.

- Corporate lens: Reorient channel strategies—capture value from midstream entities like PE and distributors.

Money, Risk, and Financial Behavior

For decades, farmers have operated under tight credit constraints and opaque financing structures. Now, fintech innovations—such as embedded credit, revenue-based lending, crop-specific insurance, and dynamic risk repricing—are rewriting these dynamics.

“Fintech doesn’t just enable transactions; it rewires decisions.”

- Opportunity: Integrate financial models into agtech solutions to drive adoption.

- Advice to founders: Partner with lenders, co-ops, or insurers to embed financing and reduce frictions.

- Corp focus: Rethink sales strategies—beyond product, think about enabling financing to influence adoption.

The “Efficacy Stack”: Mode, Formulation, and Expression

Pathogen resistance is escalating, demanding more than incremental innovation. Novel biologicals, chemically precise formulations, microbial consortia, epigenetic triggers, and delivery platforms need to work together as an integrated stack.

- Startup insight: A new peptide is rarely enough. You need to deliver it properly—encapsulated, triggered, stable.

- Investment thesis: Platform plays that combine discovery, formulation, and delivery will outperform standalone innovations.

- Corporate opportunity: Pursue M&A or partnership strategies targeting end‑to‑end efficacy systems.

Channel Efficiency as an Operational Imperative

The ag input boom (2021–2024) culminated in channel dysfunction: oversupplied warehouses, revenue spikes, and subsequent busts, driven by fragmented visibility and coordination.

Ag input supply chains need digitization—real-time demand sensing, inventory visibility, adaptive logistics, and traceability. These systems aren’t fringe tech—they’re core resilience tools. ESG dashboards are no longer optional; they’re financial risk mitigators.

- Builder opportunity: Solutions enabling supply chain orchestration are now must-haves.

- Investor rationale: Digital tools improving capital flow and coordination at the midstream layer can reduce massive inefficiencies.

- Corporate mandate: Make supply‑chain visibility and adaptability board-level priorities. Tie them to margin resilience.

The Rise of the Global South

Traditionally, innovation flowed from North to South. That is changing. Latin America, Africa, and South Asia are emerging as sources of innovation—not just consumers. Environments characterized by climate variability, fragmented supply chains, and mobile-led adoption have become fertile grounds for rapid, local innovation.

- Entrepreneurial tip: Build locally — don't export solutions designed elsewhere. Weave local teams into product development.

- Investor angle: These regions are not beta markets; they are proving grounds—fast, local, practical, and high-impact.

- Corporate lens: See these regions as innovation labs and pipeline donors, not just sales territories.

Circular Inputs and Resource Resilience

The linear input model—extract, synthesize, distribute—can't withstand cost volatility, environmental scrutiny, or input shortages. Circular systems—biochar, on-farm nutrient loops, recycled nutrients, decentralized biomanufacturing—offer a viable alternative.

- Startup focus: Develop modular, mobile, on-farm systems for nutrient recycling.

- Investor insight: Circular resource systems are not purely climate plays; they underpin input cost resilience and independence.

- Corporate action: Rethink supply strategy to facilitate verified circular models and supply resilience.

Innovation at the Seams of Adjacent Sectors

Agtech is converging with energy, textiles, water, health, and biotech—giving rise to nascent, unnamed verticals.

- Ag waste ➝ bio-based plastics

- Pharma from crops

- Microbial energy storage

- Cotton as carbon finance trigger

These adjacent intersections are where the biggest value resides—not within siloed agtech sectors.

- Entrepreneur opportunity: Build cross-sector plays fluent in ag and at least one adjacent domain.

- Investor strategy: Look for sector bridges—energy, textile, water, health.

- Corporate action: Expand R&D horizons; don’t just acquire agtech, acquire cross-domain orchestration assets.

Emerging Signals: What’s Coming Next

AI & LLMs

From discovery platforms to agronomic decision-making, AI—including large language models—is accelerating everything. Soon, using AI in ag will not be optional; it will be assumed. (placeholder citation — confirm)

The Shrinking Middle Layer

A slowdown in Series B/C funding and corporate venturing is creating a “scale-capital” gap. Many agtech startups are stuck—too expensive for seed rounds, too early for growth equity.

Yet winners will emerge, not through speed, but through targeted capital aligned with structural leverage.

Why These Trends Matter

We’re seeing the migration of opportunity from product-centric to system-centric innovation. The quiet shifts—capital, ownership, financial structures, supply chains, health, circular inputs, cross-sector value chains—are actively rerouting how capital flows, what adoption looks like, and which power dynamics form.

Success in the coming decade will belong not to the highest-yield producers, but to those reimagining the system before others notice.