By Agroempresario.com

Despite an 86% drop in venture capital (VC) funding for biostimulants in 2024, interest in these plant-boosting inputs remains remarkably strong. According to industry leaders and new data revealed at the 2025 Salinas Biological Summit, the biostimulant sector continues to evolve and attract attention due to increasing demand for sustainable, high-efficiency agriculture.

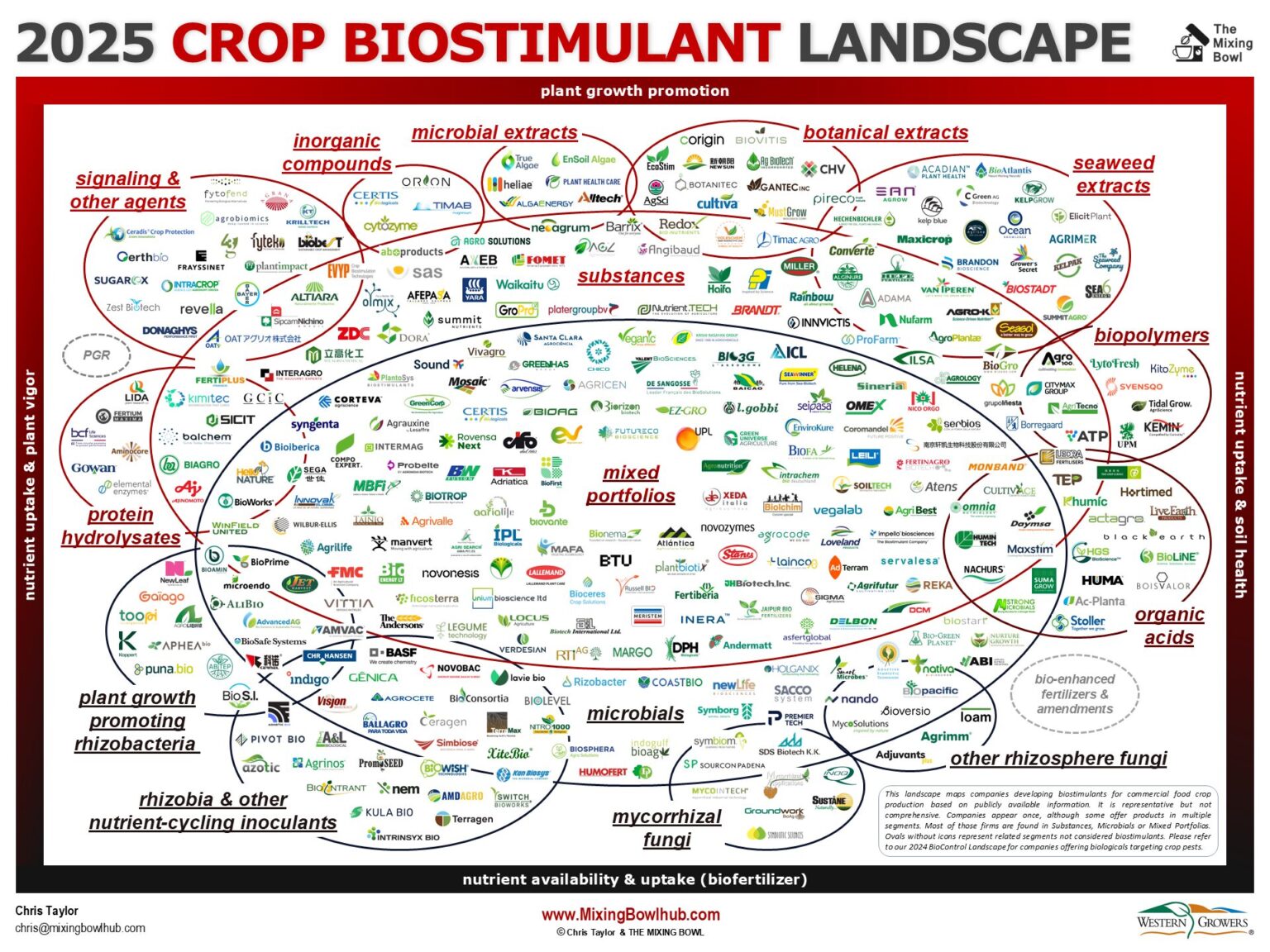

Unveiled at the June summit, The Mixing Bowl’s 2025 Crop Biostimulant Landscape identifies 350 companies across 12 ingredient categories, showing just how crowded and competitive the space has become. Even with limited funding, the momentum behind biostimulants appears unstoppable.

What Are Biostimulants and Why Are They Growing in Popularity?

Biostimulants are substances or microorganisms applied to plants or soil to improve nutrient efficiency, tolerance to abiotic stress, and overall crop quality. Unlike fertilizers, which provide nutrients, or biocontrols, which fight pests, biostimulants stimulate natural processes in the plant itself.

These biological solutions are gaining popularity as agriculture faces increasing pressure to reduce chemical inputs due to environmental and human health concerns. Regulations on conventional pesticides and fertilizers are tightening, making biostimulants a promising alternative for farmers seeking yield resilience and sustainability.

Chris Taylor, partner at The Mixing Bowl, notes:

"Interest in biostimulants has been extraordinary. However, the sector remains difficult to navigate due to vague definitions, regulatory gaps, and overlapping functionalities."

VC Funding in 2024: A Major Dip, But Not a Death Knell

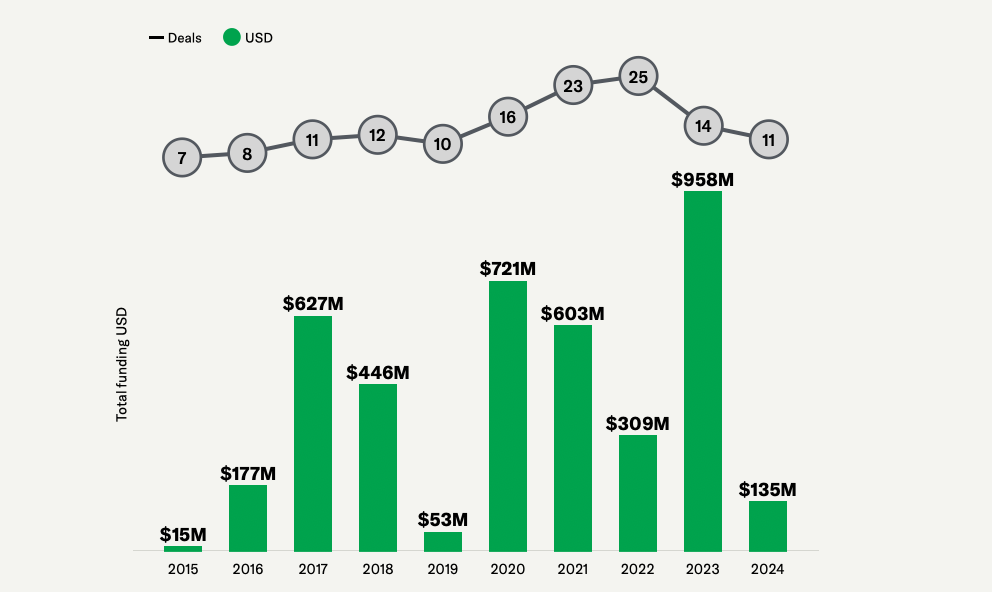

According to AgFunder data, funding to biostimulant startups dropped 86% in 2024, totaling only $135 million, with over 50% going to early-stage startups. This mirrors a broader VC contraction across the agrifoodtech industry and beyond, due to global economic uncertainty and geopolitical instability.

Still, industry players suggest that the drop is more about timing than disinterest. The long-term outlook remains promising.

"We’re seeing a maturing market. Consolidation and strategic partnerships are increasing, which is typical as new industries grow past early exuberance," says Taylor.

A Decade of Growth and Resilience

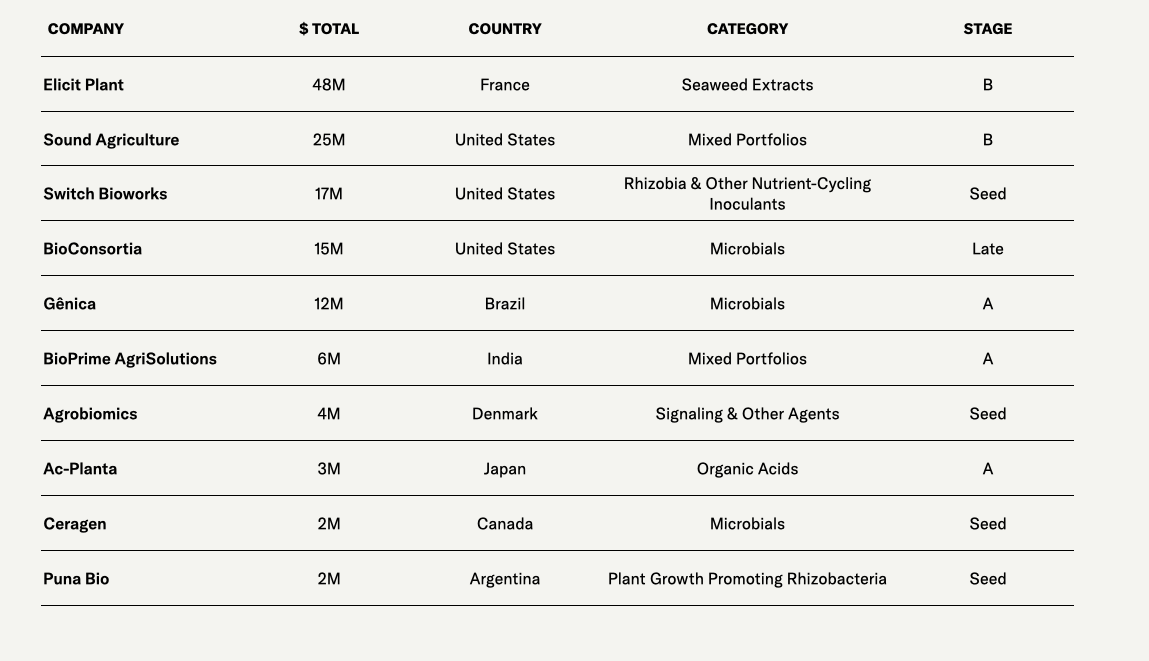

Since 2015, companies featured in the new market map have raised a combined $4.2 billion. Among them, 50 startups have publicly disclosed funding rounds totaling 159 transactions.

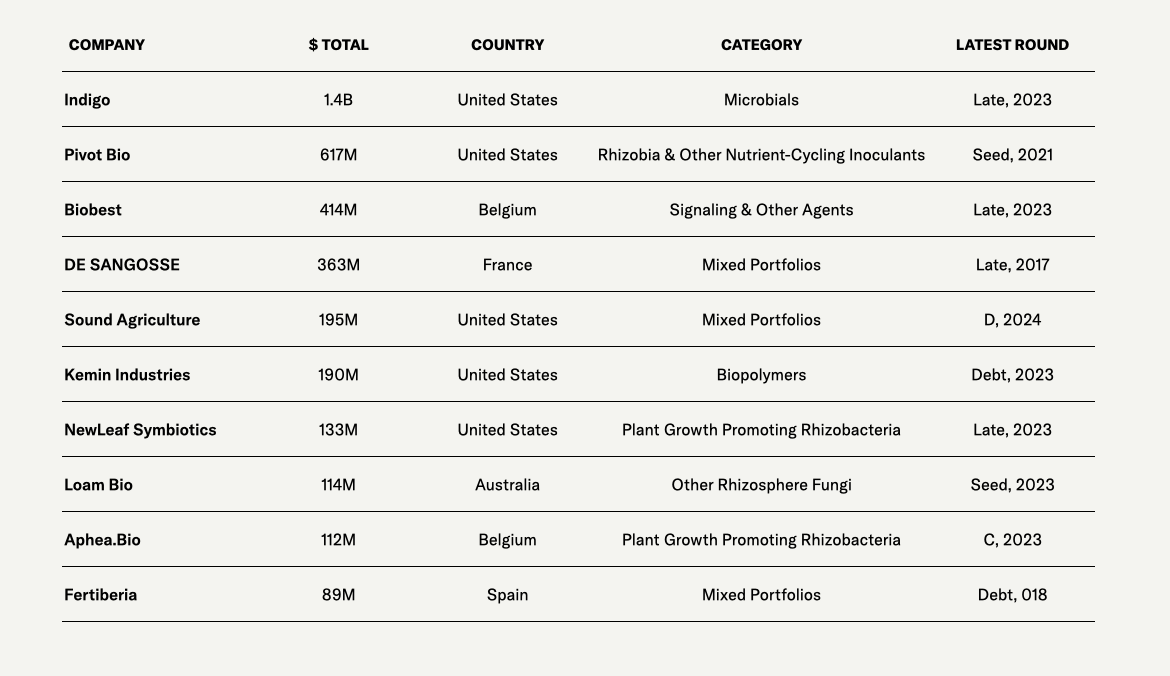

Biostimulant funding peaked in 2023 with $958 million, driven by massive late-stage rounds like Biobest’s $391 million and Indigo’s $270 million. Pivot Bio also made headlines earlier with a $430 million Series D.

Yet, deal activity peaked in 2022 (25 deals) and fell to pre-pandemic levels in 2024, suggesting a recalibration in investment strategies, rather than a decline in potential.

Geographic Distribution: US Dominates, India and France Emerging

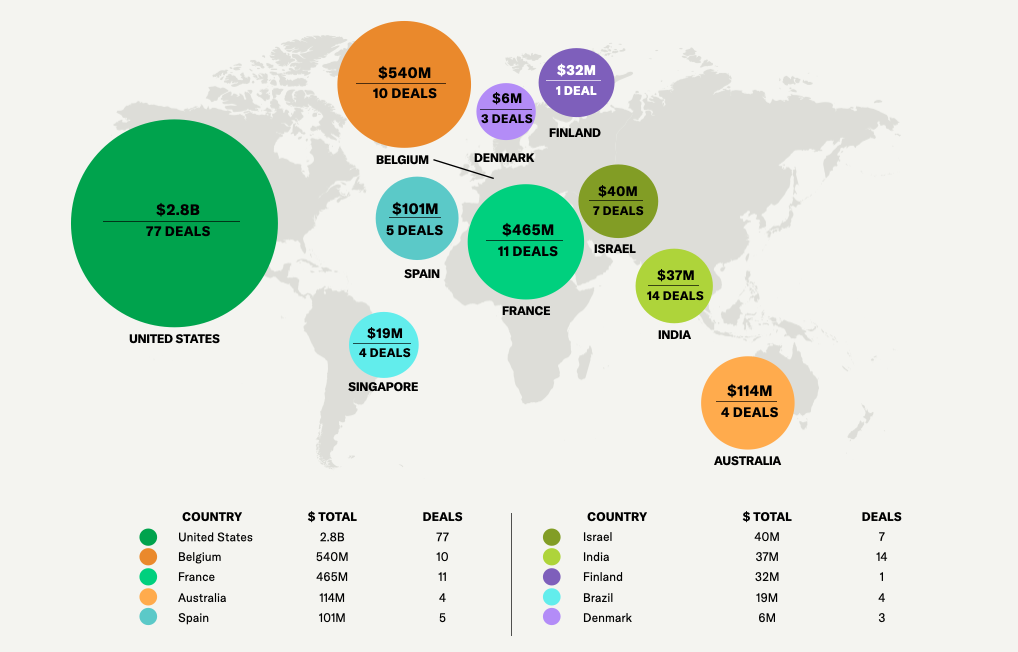

The United States is the clear leader in biostimulant funding, accounting for 67% of global investment since 2012. Belgium and France follow in total capital raised.

In terms of deal count, India ranks second, despite ranking seventh in total funding. France and Belgium also show strong deal activity, indicating regional clusters of innovation.

Challenges in Regulation and Product Differentiation

One of the biggest obstacles in the biostimulant space is terminology confusion and inconsistent regulations. While the European Union and Brazil have established definitions for biostimulants, the United States has yet to create a uniform standard.

During the Salinas summit, Dr. Pam Marrone noted that the Plant Biostimulant Act, recently reintroduced in the U.S. Congress, aims to provide a federal definition and streamline the approval process.

Currently, 29 U.S. states are expected to initiate or continue biostimulant regulation efforts in 2025. California’s Senate Bill 1522, passed last year, defines biostimulants as substances that support a plant’s natural nutrition processes, independent of nutrient content.

Limited Ingredients, Complex Combinations

Biostimulant formulations typically include a narrow range of active ingredients—like seaweed extracts, protein hydrolysates, organic acids, and specific microbial strains. These are often used in combination, making it difficult to differentiate between products.

"It's hard to differentiate biostimulants because many use the same few ingredients in different blends," says Taylor. "Clarity from regulators and more transparent messaging from manufacturers are critical."

Producers also face challenges evaluating products, as their decisions depend on crop type, farming system, location, and risk tolerance.

What’s Next for Biostimulants?

Despite funding fluctuations, the underlying drivers for biostimulant adoption are growing stronger. The need for climate-resilient crops, soil regeneration, and reduced chemical dependence all point to continued biostimulant growth.

Key areas for future development include:

- New active ingredients, including RNAi-based solutions

- Improved shelf life and ease of application

- Efficacy trials and real-world validation

The sector is also likely to see ongoing mergers, acquisitions, and strategic alliances, as larger ag companies look to expand their biological portfolios, and startups seek go-to-market support.

"The market will find its balance," concludes Taylor. "But the interest in sustainable, biological crop solutions is not going away."

A Crowded, Complex, but Promising Space

Biostimulants sit at the intersection of science, sustainability, and scalability. While 2024 may have seen a dramatic drop in VC funding, the sector is far from declining. Instead, it's entering a more selective, data-driven phase that rewards clarity, innovation, and collaboration.

As global agriculture continues to shift toward low-input, high-output systems, biostimulants will remain a critical piece of the puzzle. For investors, startups, and farmers alike, now is the time to refine, reframe, and reimagine the role of biostimulants in building a resilient food system.